Top 5 Cross-Border Remittance Solutions for Businesses

Mekari Insight

- Cross-border remittance solutions are technology-driven services that enable businesses to send international payments more efficiently by reducing transfer costs and settlement time.

- These international solutions simplify global transactions by providing faster processing, better exchange rate transparency, and streamlined payment workflows.

- Mekari Expense is a spend management software that includes cross-border remittance solutions capabilities to help companies manage international transfers, control spending, and improve financial operations across multiple countries.

Businesses of all sizes now need to send and receive money across borders and nations amid the explosive growth of global and international trade.

UNCTAD reports that global trade hit a record $35 trillion in 2025, growing 7% or around 2.2 trillion from the previous year (2024).

However, the traditional banking system struggles to keep pace, because it was never designed for speed or cost-efficiency.

This traditional system also imposes hidden fees that quietly erode margins, force 2–5 business day settlement waits, expose businesses to fluctuating exchange rates, and create compliance complexity across diverse regulatory regimes.

Cross-border remittance solutions emerge as the game-changing answer. These modern platforms and payment rails enable businesses to move money internationally faster, cheaper, and fully transparent.

This article will guide you to understand what cross-border remittance solutions are, how they work behind the scenes, the main types available, key use cases for businesses, and practical steps to choose the best one for your operations.

What is a Cross-Border Remittance Solution?

Cross-border remittance is the international money transfer across different countries, whether for personal use or business purposes.

Generally, this international payment process involves currency conversion, intermediary banks or payment networks, and compliance with cross-border regulations like AML and KYC checks.

As mentioned above, cross-border remittances serve two main purposes:

- Personal remittance: Transfers primarily made by individuals with typically smaller amounts sent regularly through consumer apps or money transfer operators (e.g., migrant workers supporting families back home).

- Business remittance: Transfers between companies with larger amounts processed for enterprise needs, such as account payables and supplier invoices, global payroll processing, and B2B payments or intercompany transfers.

Read More: Best 10 Accounts Payable Software for Large Businesses in 2026

To cover those needs, especially the business one, many cross-border remittance solutions have emerged.

Cross-border remittance solution refers to a technology-driven financial service or platform that enables individuals or businesses to send money, make payments, or transfer funds securely between different countries.

In modern context, these solutions are not limited to bank wires, but also include digital platforms, APIs, payment networks and gateways, and fintech services.

These platforms and services matter most for companies because businesses increasingly rely on fast, reliable cross-border payments, as the global B2B payments market size reached $97.88 trillion in 2025 and is projected to grow to $109.39 trillion in 2026 and $282.48 trillion by 2034.

With such massive volumes at stake, adopting the right cross-border remittane solution becomes essential for companies to stay competitive in global markets.

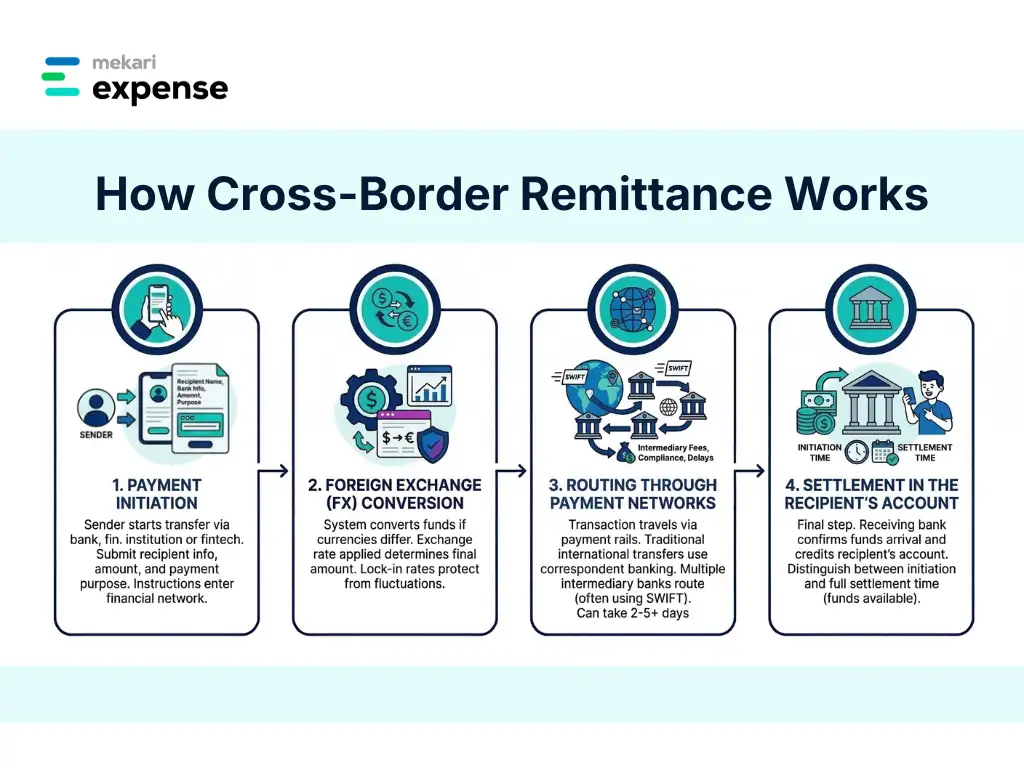

How Cross-Border Remittance Works

Understanding how cross-border remittance works helps businesses and finance teams better anticipate transfer times, manage costs, and choose the right payment solution for international transactions.

The process generally follows several key stages, from initiating the payment to settling the funds in the recipient’s account.

1. Payment Initiation

The process begins when the sender initiates a payment through a bank, financial institution, or fintech platform. At this stage, the sender provides key transaction details, such as:

- Recipient name and bank account information

- Destination country and currency

- Transfer amount

- Payment purpose (often required for compliance)

Once submitted, the payment instruction will enter the financial network for processing.

2. Foreign Exchange (FX) Conversion

If the sender and recipient use different currencies, the system must convert the funds through a foreign exchange (FX) process.

The exchange rate applied at this stage determines how much the recipient ultimately receives. Some providers lock in the FX rate at the moment the transaction is initiated, protecting the sender from currency fluctuations that may occur during processing.

Without this lock-in mechanism, sudden changes in exchange rates can affect the final amount delivered.

3. Routing through Payment Networks

After the payment is initiated and the currency is determined, the transaction must travel through financial infrastructure known as payment rails.

In traditional international transfers, banks rely on correspondent banking networks. This means that if the sender’s bank does not have a direct relationship with the recipient’s bank, the payment is routed through one or more intermediary banks that hold accounts with each other.

These transactions are commonly communicated through the SWIFT messaging network, which securely transmits payment instructions between banks worldwide. However, SWIFT itself does not move the money—it only sends the message that instructs banks to transfer funds.

Because multiple intermediary banks may be involved, this model often introduces:

- Additional processing fees

- Compliance checks at each institution

- Delays in settlement

As a result, traditional international transfers can take 2–5 business days or longer with extra fees applied in each transaction.

4. Settlement in the Recipient’s Account

The final step of the cross border remittance’s process is settlement, when the receiving bank confirms that the funds have arrived and credits the recipient’s account.

However, there may be a delay between when a payment is sent and when it is fully settled. Therefore, it is important to understand the time needed for each transfer and distinguish them:

- Transaction time: when the payment instruction is sent

- Settlement time: when the funds are actually available to the recipient

Even if the transaction is initiated instantly, settlement may take longer depending on intermediary banks, compliance checks, and time zone differences.

How Modern Remittance Solutions Improve the Process

Cross-border remittance solutions are designed as alternatives to reduce the inefficiencies of traditional correspondent banking systems.

Instead of routing payments through multiple intermediary banks, modern platforms may use:

- Direct payment networks that connect financial institutions in different countries

- Local ACH integrations that allow payments to be processed through domestic clearing systems

- API-based fintech infrastructure that connects businesses directly to global payment rails

By shortening the transaction path, these systems can significantly reduce transfer time, lower costs, and improve transparency.

Many modern solutions also provide real-time tracking and payment confirmation, allowing businesses to monitor the status of each transfer from initiation to settlement.

This visibility helps finance teams reconcile international payments more efficiently, maintain better control over cross-border cash flow, and seamlessly feed data into their accounts receivable cash application workflows.

Cross-Border Remittance Solutions Types

Businesses today can choose from several types of cross-border remittance solutions, each with different infrastructure, costs, and settlement speeds.

Understanding these options helps organizations select the most efficient method for sending international payments based on their operational needs.

1. Bank Wire Transfers (SWIFT)

Bank wire transfers are the most traditional method for sending money internationally. These transfers typically rely on the SWIFT network, which allows banks around the world to exchange secure payment instructions.

When a bank does not have a direct relationship with the recipient’s bank, the payment is routed through one or more correspondent banks.

Each intermediary bank processes the transaction before passing it along to the next institution until it reaches the final destination.

While SWIFT transfers are widely accepted and reliable, they often come with several limitations:

- Longer settlement times, typically ranging from 2–5 business days

- Multiple intermediary fees, which increase the overall transfer cost

- Limited transparency, as senders may not always see where the payment is during processing

Despite these drawbacks, SWIFT wire transfers remain a common option for large-value international transactions and payments between established banking institutions.

2. Fintech / Digital Payment Platforms

Fintech and digital payment platforms have emerged as modern alternatives to traditional cross-border bank transfers.

These solutions typically use API-based infrastructure, direct payment networks, and local banking integrations to enable faster, more transparent, and often lower-cost international transfers.

Common advantages of this fintech-based international remittance solutions include:

- Faster transfer speeds, often enabling same-day or near-instant international payments

- Lower transaction costs, by reducing or eliminating intermediary banks

- Transparent FX rates and fees, allowing businesses to see the full cost of a transaction upfront

- Real-time payment tracking, improving visibility for finance teams

- Seamless integration with business systems, such as accounting or expense management platforms

Several digital payment platforms have built their services around those advantages, including:

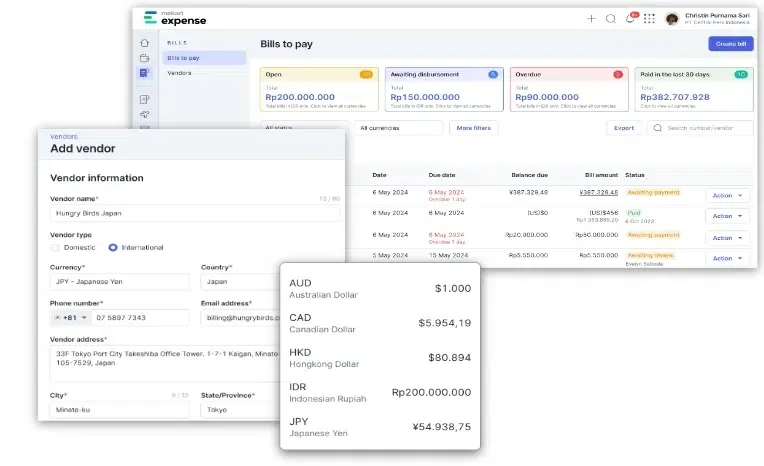

Mekari Expense

Mekari Expense is a spend management system that includes international remittance solutions capabilities, allowing companies to send cross-border payments while maintaining centralized financial visibility and control. This cross-border remittance solution includes several key features such as:

- Seamless international payments: Send funds to overseas vendors or partners directly from the platform without switching between multiple banking systems.

- Accurate exchange rates: Currency conversion uses reliable real-time exchange rates to help ensure payment accuracy.

- Transparent fees: All exchange rates and transaction fees are shown upfront before the payment is processed.

- Real-time status tracking: Finance teams can monitor the payment status from submission to settlement.

PayPal

PayPal is a digital payment platform that enables individuals and businesses to send and receive international payments, often used for e-commerce and freelance transactions.

This global payment platform is widely adopted due to its strong payment security, fast transfers in many corridors, and extensive global user base.

Wise

Wise is a fintech platform specializing in international money transfers with transparent fees and real exchange rates, often using local banking networks to reduce transfer costs.

This international money transfer service is known for its low fees, mid-market exchange rates, and faster settlement compared to many traditional bank wires.

Airwallex

Airwallex is a financial platform that offers multi-currency accounts, cross-border payments, and financial APIs designed for businesses operating internationally.

This global payment infrastructure enables companies to send and receive international payments with competitive FX rates and scalable payment capabilities.

MoneyGram

MoneyGram is a global money transfer service that enables international remittances through digital platforms as well as an extensive network of physical locations worldwide.

This cross-border remittance solution is recognized for its wide global coverage, fast transfer options, and accessibility through cash pickup locations in many countries.

3. Multi-currency Accounts

Multi-currency accounts allow businesses to hold, send, and receive funds in multiple currencies from a single account. Instead of converting money immediately during each transaction, companies can store balances in different currencies and convert them only when needed.

This approach provides several advantages for international businesses:

- Reduced FX conversion frequency, which can lower foreign exchange costs

- Greater control over exchange timing, allowing companies to convert funds when rates are favorable

- Simplified global payments, since businesses can pay international partners directly in their local currencies

Multi-currency accounts are particularly useful for companies that regularly transact with suppliers, partners, or customers in different countries.

Read More: Best AI for Accounts Payable Solutions for Businesses

4. Local Payment Rails (ACH / Real-Time Networks)

Another modern approach to cross-border remittance is connecting directly to local payment rails in the destination country.

These international transfer solutions allow international payments to be processed through domestic clearing networks instead of traditional correspondent banking chains.

Some countries have developed their own domestic real-time payment networks that can be used as local rails for international transactions, such as:

- PayNow in Singapore

- UPI (Unified Payments Interface) in India

- Bacs Payment Schemes Limited in the United Kingdom (UK)

By routing payments through these local infrastructures, transfers can often achieve near-instant or same-day settlement while significantly reducing intermediary fees.

Key Use Cases for Cross-Border Remittance Solutions

Cross-border remittance solutions support a wide range of international financial activities, from operational payments to revenue management. Some of the most common use cases include:

- International supplier payments: Pay overseas vendors and manufacturers in their local currency without delays that could disrupt procurement or supply chain operations.

- Accounts payable automation: Integrate cross-border payments directly into AP workflows to reduce manual processing and ensure timely settlement with international vendors.

- Global payroll & contractor payments: Pay remote employees, freelancers, or contractors across multiple countries on time while maintaining predictable FX costs.

- E-commerce & marketplace collections: Accept payments from international customers and settle funds in the business’s home currency more efficiently.

- Cross-border B2B invoicing: Streamline accounts receivable from foreign clients with automated FX conversion and easier payment reconciliation.

- Revenue repatriation: Transfer earnings from overseas subsidiaries or regional operations back to the parent company with greater efficiency and visibility.

- Migrant worker remittances: Enable diaspora communities to send money back to their families through faster and more affordable international transfer services.

Read More: Top 7 Procurement Automation Software to Streamline Procurement Cycle

Key Challenges in Cross-Border Remittances

Despite enabling global transactions, cross-border remittances still present several operational and financial challenges for businesses.

- High fees & hidden costs: Correspondent bank charges, intermediary fees, and unfavorable FX markups can significantly reduce the value of a transaction. For example, the average international bank wire from Indonesia costs around $40 per transaction, excluding additional FX margins.

- Slow settlement times: Traditional SWIFT-based transfers often take 2–5 business days to settle, which can create uncertainty for businesses that rely on timely payments to suppliers or partners.

- Exchange rate volatility: Currency fluctuations between the time a payment is initiated and when it is settled can affect the final amount received by the beneficiary.

- Compliance & regulatory complexity: Each country enforces different AML (Anti-Money Laundering), KYC (Know Your Customer), and reporting requirements. Failure to comply with these regulations can result in delays, blocked transactions, or financial penalties.

- Limited transparency: Businesses may not always have visibility into where their payment is within the processing chain, making it difficult to track transactions or resolve issues quickly.

- Banking access gaps: Some regions still have limited correspondent banking relationships, which can make it difficult or expensive to send money through certain international payment corridors.

How to Choose the Right Cross-Border Remittance Solution

With many providers offering international remittance solutions, selecting the right solution requires evaluating several operational and financial factors.

Businesses should assess the following criteria to ensure the cross-border payment platform aligns with their transaction needs, cost expectations, and compliance requirements.

1. Coverage & Corridors

One of the first considerations is whether the cross-border remittance platform supports the countries, currencies, and payment corridors your business frequently uses.

Some providers offer strong coverage in specific regions but limited access in others, which may affect your ability to send or receive payments smoothly.

Solutions with broader corridor coverage can reduce the need to manage multiple payment providers across different markets.

2. Cost Structure

When evaluating costs, it is important to look beyond the advertised transfer fee.

The total transaction cost often includes several components, such as:

- FX margins

- Transfer fees

- Intermediary bank charges

- Receiving bank fees.

Comparing the full cost structure helps businesses understand the actual value of a transaction and avoid hidden expenses that can accumulate over time.

3. Speed & Settlement Time

Payment speed is another critical factor in choosing international remittance solutions, particularly for businesses that rely on timely supplier payments, payroll processing, or international invoicing.

Traditional bank transfers may take several business days to settle.

Some modern platforms provide same-day or near real-time settlement for specific payment corridors by connecting directly to local payment networks.

Read More: Top 9 OCR Invoice Scanning Software: Cut Costs by 78%

4. Compliance & Licensing

Cross-border payments are heavily regulated, making compliance an essential consideration.

Businesses should verify that the provider is properly licensed and regulated in both the sending country and key destination markets.

Working with regulated platforms helps ensure compliance with financial regulations such as AML and KYC requirements, reducing the risk of blocked transactions or legal issues.

5. Integration Options

For organizations that process frequent international payments, integration capabilities can significantly improve operational efficiency.

Some platforms offer API integrations, batch payment uploads (such as Excel files), or dedicated dashboards for managing multiple transactions.

These features allow finance teams to integrate cross-border payments directly into their accounting, ERP, or expense management systems.

6. Transparency & Tracking

Payment visibility is essential for managing international cash flow. A good remittance solution should allow both the sender and recipient to track payment status in real time, from initiation to final settlement.

Greater transparency makes it easier to identify delays, confirm payment delivery, and resolve potential issues quickly.

7. Customer Support

Reliable customer support becomes especially important when handling high-value B2B international transactions. Delays or technical issues can disrupt operations, so businesses should consider whether the provider offers responsive support channels.

Cross-border remittance solution providers that offer dedicated account management or specialized support for business clients can help resolve payment issues more quickly and minimize operational disruption.

Integrated Solution for Business Cross Border Remittance

As global transactions become more common, businesses need payment solutions that are not only fast and cost-efficient but also fully integrated into their financial workflows.

Instead of managing international transfers separately from expense and financial management systems, companies increasingly rely on unified platforms that streamline cross-border payments. In this case, Mekari Expense excels as the best solution.

Mekari Expense is a spend management software which serves as remittance management software also, enabling businesses to send cross-border payments more efficiently while maintaining full visibility and control over financial processes.

By integrating international transfers into this centralized spend management platform, finance teams can manage global payments without switching between multiple tools or banking interfaces.

Key advantages of using International Remittance in Mekari Expense include:

- Complete transparency: All fees and exchange rates are shown upfront, ensuring businesses know the exact payment value with no hidden charges.

- Global financial control: Monitor exchange rates, transaction fees, and payment statuses in real time to maintain better visibility over international cash flow.

- Built-in compliance: Every transaction follows the company’s internal approval workflow, helping reduce the risk of errors or unauthorized payments.

- Time-saving automation: Payment submissions, approvals, and transaction tracking are automated, eliminating unnecessary manual processes.

- Audit-ready reporting: All transaction records are securely stored and can be accessed anytime for accurate financial reporting and audit preparation.

- Integrated financial system: Payment data is automatically synchronized with Mekari Jurnal, enabling a more efficient end-to-end financial workflow.

By combining cross-border remittance capabilities with spend management features, Mekari Expense’s international remittance helps businesses manage international payments more efficiently while maintaining better financial control.

References

Xendit. “Cross-Border Payments Feel Too Complex? Here’s How to Simplify Them.”

AFP. “Cross-Border Payments.”

FAQ

1. Is cross-border remittance the same as an international bank transfer?

1. Is cross-border remittance the same as an international bank transfer?

Not exactly. While international bank transfers are one method, modern cross-border remittance solutions include fintech platforms, APIs, and payment networks that offer faster settlement and lower fees.

2. How does Mekari Expense support cross-border remittance for businesses?

2. How does Mekari Expense support cross-border remittance for businesses?

Mekari Expense offers an integrated international remittance feature that allows businesses to send global payments with transparent fees, automated approvals, and real-time transaction tracking.

3. Why should companies use a cross-border remittance solution?

3. Why should companies use a cross-border remittance solution?

A cross-border remittance solution helps businesses send international payments faster, with greater transparency on fees and exchange rates. It also streamlines approval workflows, improves financial control, and reduces the risk of errors in global transactions.